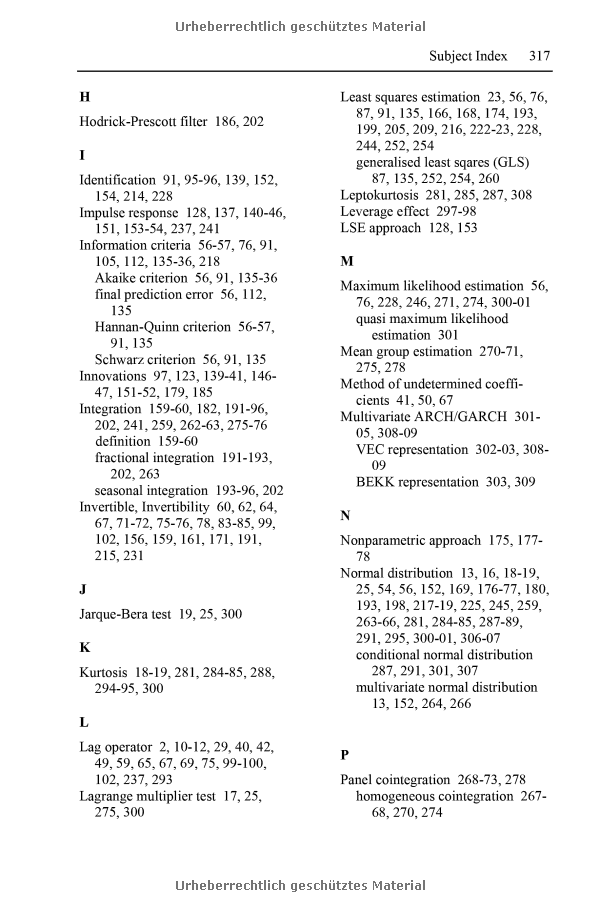

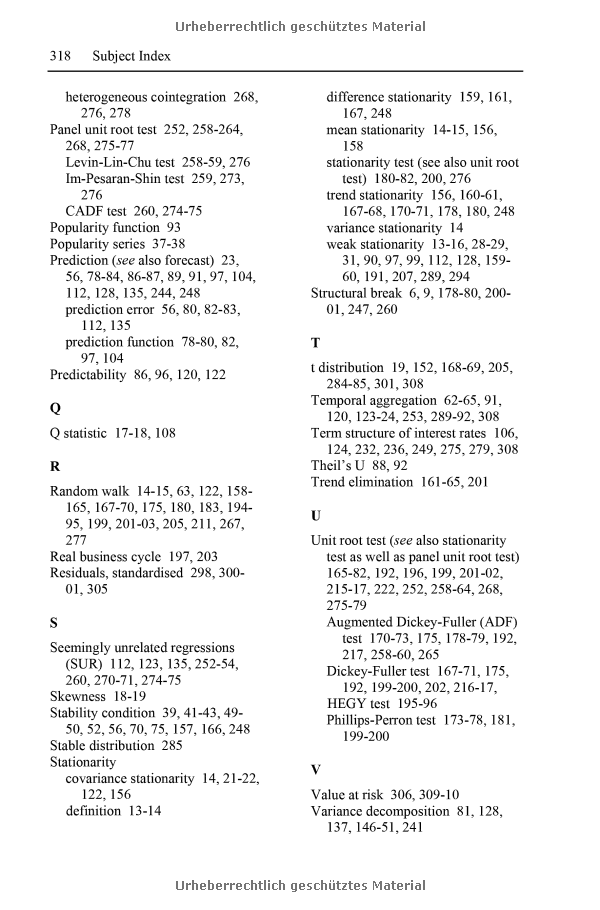

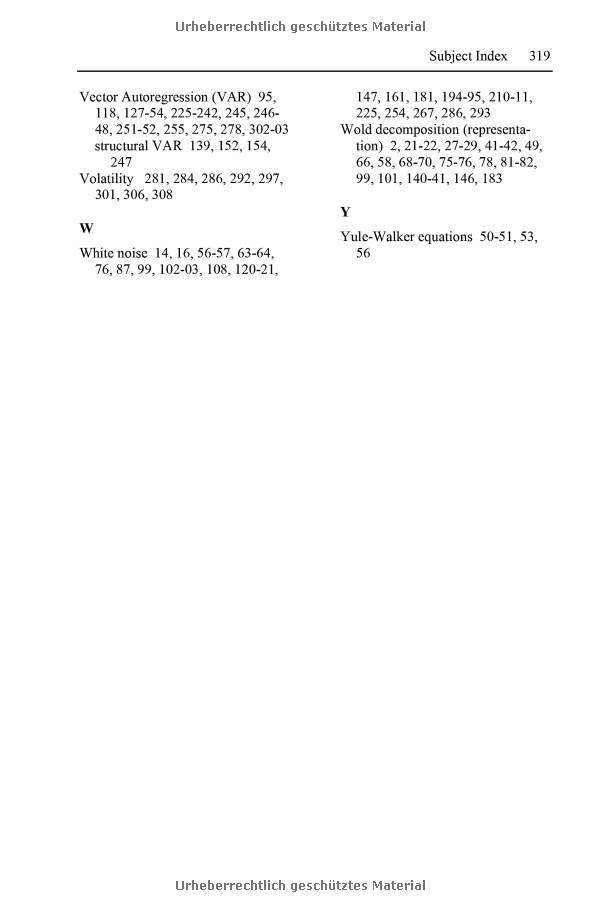

Introduction to Modern Time Series Analysis(Springer Texts in Business and Economics)

数量经济学

¥

663.00

售 价:

¥

530.00

优惠

平台大促 低至8折优惠

发货周期:通常付款后3-5周到货!

出版时间

2014年11月09日

装 帧

平装

页 码

320

开 本

9.2 x 6.1 x 0.6 cm

语 种

英文

版 次

2

综合评分

暂无评分

- 图书详情

- 目次

- 买家须知

- 书评(0)

- 权威书评(0)

图书简介

This book presents modern developments in time series econometrics that are applied to macroeconomic and financial time series, bridging the gap between methods and realistic applications. It presents the most important approaches to the analysis of time series, which may be stationary or nonstationary. Modelling and forecasting univariate time series is the starting point. For multiple stationary time series, Granger causality tests and vector autogressive models are presented. As the modelling of nonstationary uni- or multivariate time series is most important for real applied work, unit root and cointegration analysis as well as vector error correction models are a central topic. Tools for analysing nonstationary data are then transferred to the panel framework. Modelling the (multivariate) volatility of financial time series with autogressive conditional heteroskedastic models is also treated.

本书暂无推荐

本书暂无推荐

看了又看

- 上一个