Interest Rate Derivatives Explained: Volume 2:Term Structure and Volatility Modelling(Financial Engineering Explained)

利率衍生物解释 第2卷:期限结构与波动性建模

政治经济学

¥

458.75

售 价:

¥

367.00

优惠

平台大促 低至8折优惠

发货周期:预计8-10周发货

作 者

出 版 社

出版时间

2017年11月24日

装 帧

精装

页 码

248

语 种

英文

综合评分

暂无评分

- 图书详情

- 目次

- 买家须知

- 书评(0)

- 权威书评(0)

图书简介

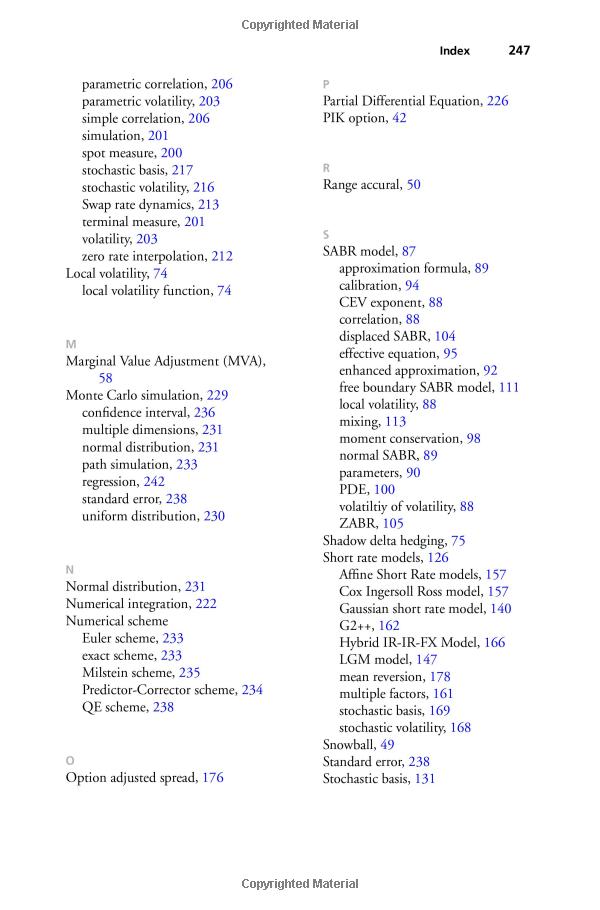

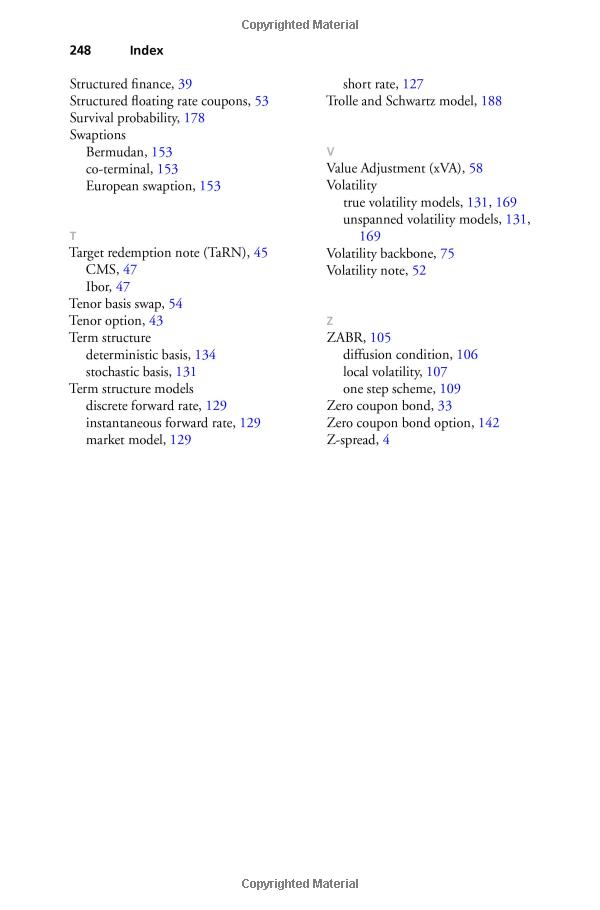

This book on Interest Rate Derivatives has three parts. The first part is on financial products and extends the range of products considered in Interest Rate Derivatives Explained I. In particular we consider callable products such as Bermudan swaptions or exotic derivatives. The second part is on volatility modelling. The Heston and the SABR model are reviewed and analyzed in detail. Both models are widely applied in practice. Such models are necessary to account for the volatility skew/smile and form the fundament for pricing and risk management of complex interest rate structures such as Constant Maturity Swap options. Term structure models are introduced in the third part. We consider three main classes namely short rate models, instantaneous forward rate models and market models. For each class we review one representative which is heavily used in practice. We have chosen the Hull-White, the Cheyette and the Libor Market model. For all the models we consider the extensions by a stochastic basis and stochastic volatility component. Finally, we round up the exposition by giving an overview of the numerical methods that are relevant for successfully implementing the models considered in the book.

本书暂无推荐

本书暂无推荐

看了又看

- 上一个